New Zealand broadband market in 2014

New Zealand is close to halfway through an ambitious project to boost broadband speeds nationwide. How is the broadband market shaping up?

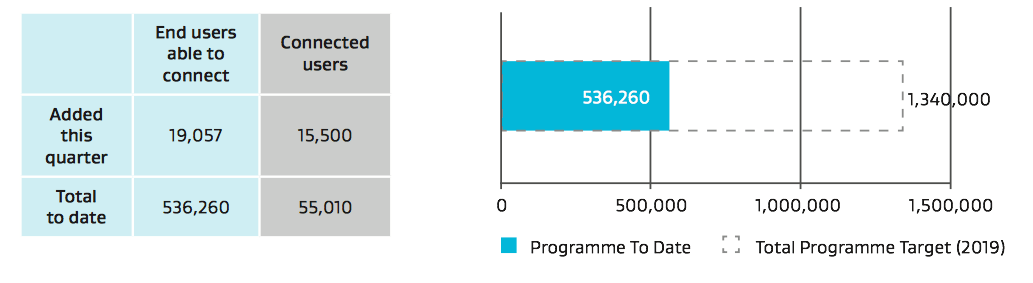

By the end of 2019 the first stage of the government-sponsored Ultrafast Broadband project will be complete. UFB will connect the 75 percent of the population living in urban areas to a fibre network. A second stage will add roughly another 5 percent of the population to the network.

Meanwhile the Rural Broadband Initiative will boost speeds for people living in country areas.

The Ministry of Business, Innovation and Employment’s September quarterly report says 80 ISPs offer fibre.

Follow the money

That’s a lot of service providers for a small country. Not all are prospering.

Spark, New Zealand’s biggest internet service provider, doesn’t make money from broadband.

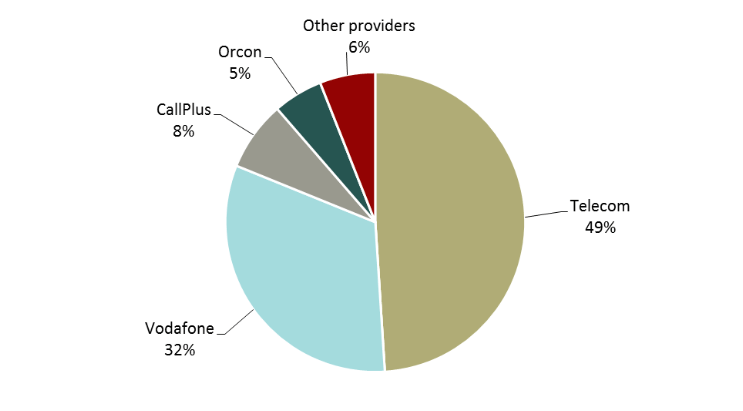

A panel in Spark’s 2014 annual report says the company has 669,000 connections. That’s up 20,000 on a year earlier. Spark has a 49 percent share of the broadband market — roughly half of all New Zealanders connect online using Spark.

During the year Spark’s broadband revenue declined 2.4 percent from $291 million to $284 million. The company reports broadband made a $12 million loss.

Intense competition

In its annual report Spark puts the fall down to: “a strategic decision to hold share in the broadband market by re-pricing our consumer plans”. In other words — intense price competition.

Vodafone is New Zealand’s second largest ISP. According to the Commerce Commission’s 2014 monitoring report, Vodafone has a 32 percent broadband market share.

Unlike most of its rivals, Vodafone operates its own cable network in parts of Wellington and Christchurch.

Vodafone New Zealand doesn’t break out detailed financials. That makes it difficult to know how well it does in broadband.

Vodafone first loss in 13 years

In 2014 Vodafone NZ as a whole posted a $27.9 million loss down from a $55.9 million profit a year earlier. The figures come from financial statements lodged with the Companies Office. That means Vodafone New Zealand made its first loss in 13 years.

New Zealand’s third largest ISP is the CallPlus Group. The group owns the CallPlus, Slingshot, Orcon and Flip brands. The Commerce Commission estimates the group accounts for 13 percent of broadband connections. When the company acquired Orcon in June 2014 Chief executive Mark Callander said it had around a 15 percent market share.

CallPlus is private. There aren’t easy to find figures to estimate its business performance in the broadband market. What is know is that Orcon was losing money before CallPlus acquired it.

At the time of writing Spark, Vodafone and CallPlus make up 95 percent of New Zealand fixed-line broadband connections.

Who makes money from broadband?

We know Spark and Orcon lost money on broadband services. We don’t know if Vodafone and the rest of CallPlus are profitable. It’s reasonable to assume that even if they are in the black, at best, as a group the three ISPs break even.

This goes some way to explain why the three were quick to raise prices when the Commerce Commission increased the copper access wholesale price.

Snap is the next biggest ISP after Spark, Vodafone and CallPlus. Snap is about one-third the size of Orcon. According to the Telecommunications Development Levy allocation it has $11 million of qualified revenue compared to Orcon’s $33 million.

The last four percent

If 80 ISPs offer fibre, there are at least 75 smaller businesses sharing the last four percent or so of the broadband market. Many are regional or in a niche and serve only a few hundred customers.

This ISP market tail is where things get interesting, because while they each have a relatively small share of the market, we can reasonably assume most of them are profitable or break even.

How can we assume this? Because small ISPs rarely have access to capital. They tend to live hand to mouth. If they weren’t profitable they wouldn’t last long. Directors and business owners draw an income — sometimes a good income from the businesses.

There’s another interesting aspect to the small ISPs. They may represent the future. When some ISPs announced price rises after the Commerce Commission review of copper access prices Tuanz CEO Craig Young said:

We will watch with interest what the more agile service providers do given this is an opportunity to gain market share from the larger player.

Looking at minnows:

Snap Internet is the largest minnow. Commerce Commission figures show Snap is among the fastest growing ISPs in New Zealand. Snap started out as an independent, regional South Island ISP. In round numbers it is about one percent of the broadband market.

Industry rumour says Snap won’t stay independent for long. The word on the street is that 2degrees will acquire the business.

Snap is the kind of agile service provider Young had in mind.

Gigatown

Despite being tiny it has been quick to embrace fibre, it got into the market long before Spark or Vodafone. Snap was one of the first ISPs to offer Dunedin residents Gigatown pricing. It was also quick to raise prices after the Commerce Commission announcement.

Tiny Snap is also a solid performer. TrueNet describes it as a market leader.

Snap doesn’t file public results. However, I discussed margins and profitability with the company this time last year. Snap told me the business makes a profit with a margin of “better than four percent, not as good as 10 percent”.

Enter MyRepublic

For now the Singaporean-backed MyRepublic is a minnow. It only started selling in October. And because it only sells fibre services, it can only address a fraction of the market.

MyRepublic is small, but CEO Vaughn Baker has ambitions to be big and disruptive. The parent company in Singapore is a major player in that market and reshaped the ISP business after the city-state rolled out its fibre network.

On one level Baker’s strategy is simple. He aims to chase two niche consumer markets with special needs: gamers and online entertainment junkies. The MyRepublic’s network is optimised for gaming and streaming video.

Price as a weapon

Price is part of that strategy. MyRepublic has gone with aggressive unmetered plans at around the $100 mark. With a Chorus line costing $38 and transport provisioning for unmetered data on a fibre line costing around $40 a month, there’s little room for a margin after taking support and other overheads into account.

MyRepublic is operating on the crash through or crash model. It will either build enough momentum and pull customers away from existing ISPs to win economies of scale or it will burn through its investors cash.

At the time of writing MyRepublic isn’t profitable,

That may sound reckless. If it works the potential rewards are solid. MyRepublic is taking the fight directly to the big three ISPs.

The indie ISPs

Away from the big three, Snap and MyRepublic are what I like to think of as the indie ISPs. You might also describe them as boutique ISPs. These are small, often regional, niche businesses — in many cases the owners do everything including answering helpdesk calls from customers.

One indie ISP is Dunedin-based Wicked Networks. Wicked runs a wireless hotspot network in Dunedin and offers residential broadband services in that city. It also serves business broadband customers in Dunedin and Auckland through the Chorus network.

Small ISPs tend to have an intense focus on their specific niche. That could be as simple as being the champion for a small town or region. It can also mean specialising in, say, providing services for farmers in rural areas.

Scale

One interesting aspect of New Zealand’s broadband market is that scale doesn’t seem to help. If anything the bigger players are proportionately less profitable than the minnows.

That could be temporary. Spark’s quick repricing move after the recent Commerce Commission ruling suggests a fresh willingness to risk losing market share in return for better margins. It was a gamble that paid off with other big players making similar moves.

As New Zealanders move more to fibre, things will change again. In some ways fibre offers less scope to differentiate the basic service, so ISPs will need to find alternative approaches. MyRepublic’s decision to opitimise for gamers and streaming video is an example of this. Local and niche focus by the indies are another.

Despite profits being elusive for the big players, New Zealand’s broadband market looks in good shape. There are big, largely undifferentiated ISPs and small, focused niche players. Competition is working as it should, customers get a good deal.

Member discussion